BUYER FIT

Buyer fit controls allocation

Category, market, capacity, delivery path, account state, and campaign status are checked before a buyer receives volume.

ROUTING THROUGH SPEARPOINT X

Spear routes verified mortgage, finance, insurance, legal, and auto enquiries through SpearPoint X, using buyer fit checks, source controls, applicable exclusivity rules, and performance-weighted routing priority.

Our Partners

Spear works with selected companies across mortgage, finance, insurance, legal, and automotive acquisition, including Mortgage Research Center and Veterans United.

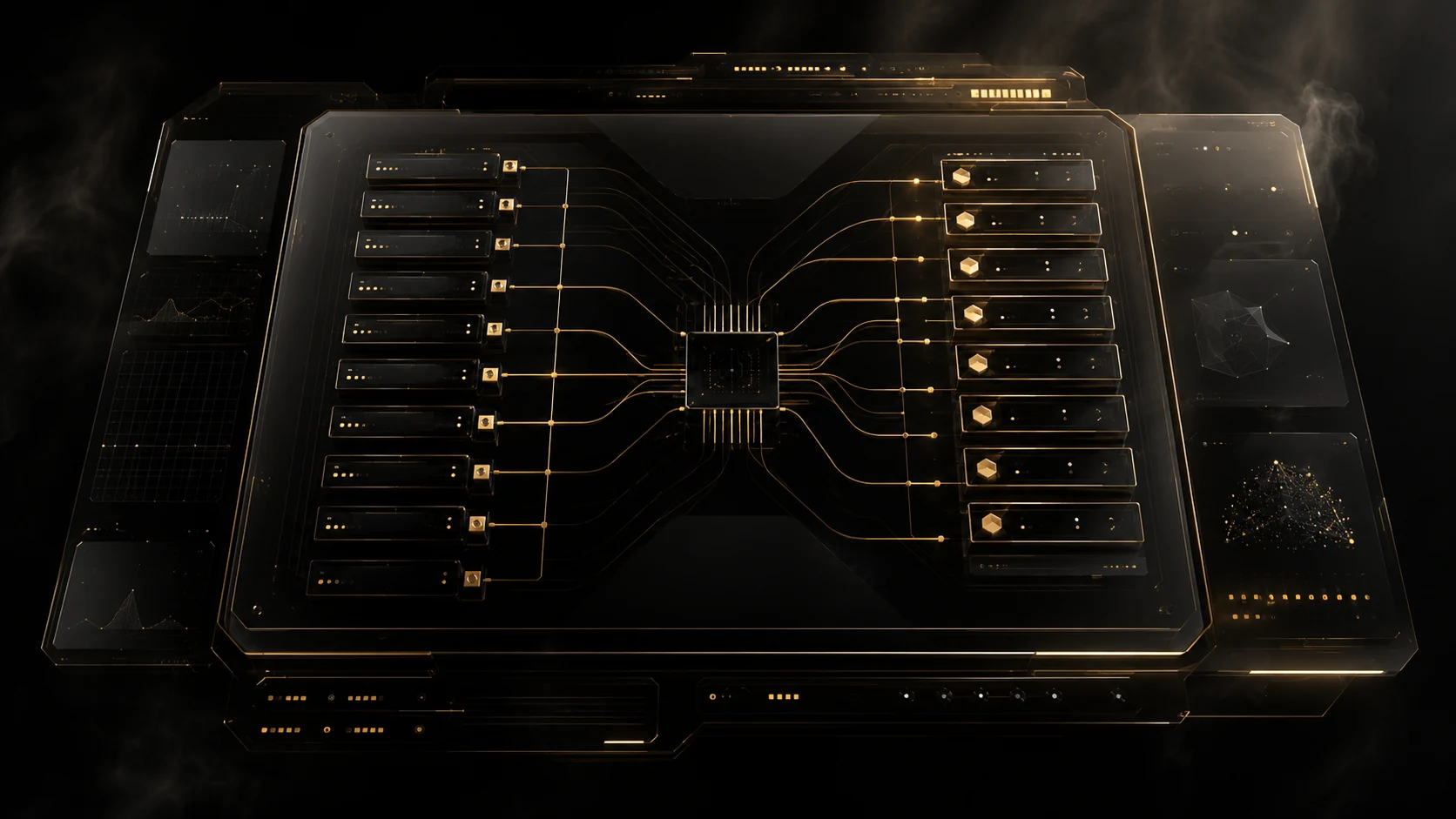

SPEARPOINT X

SPEARPOINT X / ALLOCATION ENGINE

Private routing controls, not a shared lead queue.

Buyers see the controls that protect the handoff: eligibility, priority, delivery state, and dispute posture in one routing path.

BUYER FIT

Category, market, capacity, delivery path, account state, and campaign status are checked before a buyer receives volume.

SOURCE QUALITY

Source context, consent posture, category fit, duplicate risk, and delivery compatibility stay attached to the route.

DELIVERY RECORD

Delivered records can carry timestamp, destination, state, route context, and retry posture where applicable.

DISPUTE CONTROL

Invalid-record claims, credits, resolution state, and operator notes stay attached to the original delivery record.

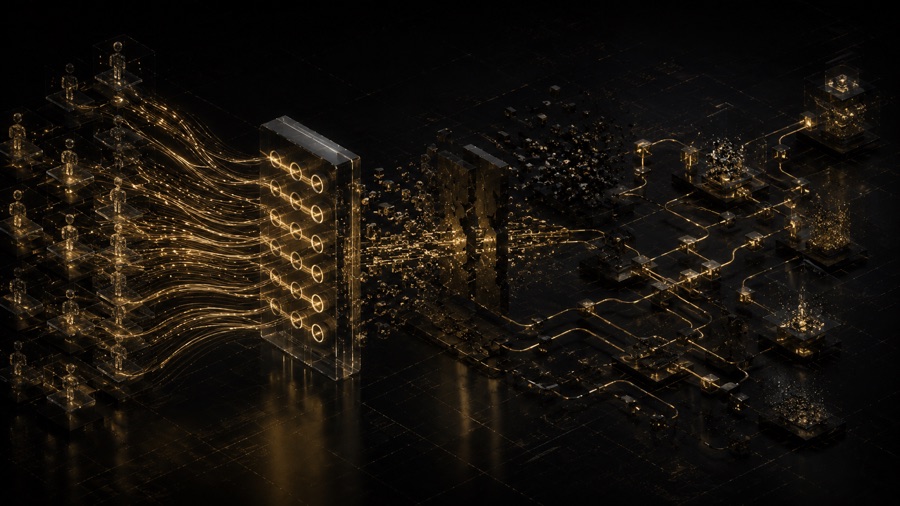

HOW ROUTING STAYS CONTROLLED

01 / VERIFY SOURCE

Consent, source context, category intent, contactability, duplicate risk, and unsupported scenarios are checked before buyer time is spent.

02 / ROUTE BY FIT

SpearPoint X evaluates category, geography, capacity, delivery state, account controls, and performance signals before allocation.

03 / RECORD THE HANDOFF

Route decisions, delivery state, deduplication, returns, credits, and feedback stay tied to the original operating record.

FOR BUYERS

Supply standard

Source, consent, category intent, and correction discipline are reviewed before supply is scaled. Only publishers that meet these controls are approved for buyer delivery.

Review publisher standardsVERTICALS

Home lending

Purchase, refinance, and home-lending enquiries where territory, consent, capacity, and handoff rules matter.

Financial services

Private lending, asset finance, and credit-related categories where source context and buyer fit need controls.

Licensed demand

Insurance enquiries that require product context, jurisdiction awareness, and careful data handling before delivery.

Intake criteria

Legal demand where case criteria, jurisdiction, consent, and claim boundaries must be clear before allocation.

Vehicle intent

Dealer, auto finance, and vehicle-intent demand where location, inventory fit, and speed-to-contact matter.

OPERATING NOTES

Operating note

Cheap shared leads turn sales reps into unpaid quality control.

Read operating note

Operating note

Controlled allocation is not a prettier word for selling leads.

Read operating note

Operating note

Slow first contact makes warm intent feel like cold outreach.

Read operating note

ACCESS REVIEW

Spear routes volume around fit, source quality, market, delivery path, compliance posture, and operating discipline.